Managed Care Introduction -- Managed Care Types -- Advantages and Disadvantages -- How to Choose the Right Plan

Challenges Concerning Medical Benefits -- Relationships to Employee Benefit Wheel -- Web Links Page -- Works Cited

Managed Care Introduction

With the ever-increasing costs of providing medical coverage, are medical benefits for employees really worth the high prices inflicted on employers? Yes! The answer is yes. According to the Integra Group, who provides financial and operational accounting consulting services to all forms of business, for every one dollar invested by the employer in an employee’s well being provides a ten dollar return on that investment (FisherVista). Before an examination of medical benefits and managed care plans can be presented, it is imperative to understand what is meant by medical benefits and managed care. Medical benefits are defined as: a payment made or an entitlement available in accordance with a wage agreement, insurance policy, or public assistance program, relating to health/medical care. Managed care, on the other hand, is a type of medical benefit. It is any system of delivering health services in which care is delivered by a specified network of doctors and hospitals that agree to comply with the care approaches established by a care-management process. Providers receive a capitated payment for providing all medically necessary care to enrollees or may be paid on a fee-for-service basis (State of California). Managed care often involves a defined delivery system of providers with some form of contractual arrangement with a health plan. Capitation is the method of payment used in managed care in which doctors or hospitals are paid a fixed amount for each person cared for, regardless of the actual number or type of services they deliver (State of California).

Employer provided medical benefits are a very important part of compensation in today’s highly competitive workforce. There are many reasons to provide medical benefits; however, the number one reason is to attract and retain competent employees, without which businesses would not survive. Surveys show that medical benefits are highly demanded by all employees. Currently, medical benefits are considered a norm as part of a basic compensation plan. In addition, each year, employees are demanding greater and greater coverage from their medical plans (Benefit News). In order to attract employees and keep them away from the competition, employers must offer a basic, if not extensive, medical benefit package. Another reason to offer medical benefits is to show concern for the employee’s welfare, an added way of attracting and retaining competent employees. If an existing or potential employee believes that the company cares about him/her, then the employee may be more inclined to stay with or join that company. When medical packages are joined by other benefits as part of a total compensation strategy, the company looks that much more appealing to both prospective employees and current ones.

Another reason to provide medical benefits is the favorable tax treatment to both the employer and the employee. Medical costs are deducted pre-tax in both instances. This means that both the employer’s and employee’s tax brackets may be lowered; thus resulting in less federal, state, and local taxes owed. An additional reason to provide medical coverage exists; it is the possibility that medical benefits will be a mandated program in the near future. The legal requirement known as Senate Bill 2 or SB2 is one of many legislative reforms that California is working on as a social measure to fix the health care problems—high costs of coverage, no regulation on cost increases, excessively high profits for insurance providers, too many Californians without insurance, etc. These legal issues will be discussed later in greater detail.

As shown medical benefits are a necessary part in all compensation packages.

The types of medical benefits and/or managed care plans available include: Health Maintenance Organizations (HMOs), Preferred Provider Plans (PPOs), Point of Service Plans (POSs), Medical Savings Accounts (MSAs), dental plans, and vision packages. Also provided will be a rundown of the pros and cons of each type of plan, and the methods of choosing the right plan to meet individual company needs. After the basics are covered, it is essential to look at the looming problems, specifically the obscene increases in benefit costs over the past few years, faced by employers and employees and the potential implications and solutions.

Managed Care Types

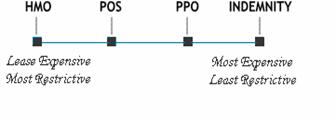

There are three main types of Managed Care in reference to employee benefits: Medical Care-- the professional treatment for illness or injury, Dental Care-- professional care for the teeth, and Vision Care-- professional care for the eyes. Managed Medical Care has three subsections: HMOs, POSs, and PPOs. For the sake of focus to attract and retain employees, the concentration of this document is Managed Medical Care due to it being the most expensive; thus, the most valuable. Individuals and employers have many plans to choose from with each offering various types of organization, service selection, and costs. Generally, the more services required to fulfill various needs and wants, the more expensive the plan.

Health Maintenance Organization

The least expensive form of managed medical care is the Health Maintenance Organization (Kaiser). Upon joining an HMO, individuals pay a fixed monthly fee, called a premium. Generally an individual pays a small co-pay, perhaps $15.00 for each visit, and $10.00 for a prescription. The range of health services vary depending on the plan, so comparison of plans is of the utmost importance. A list of doctors and hospitals is provided and a primary care physician (PCP) can be chosen from that list. The PCP is responsible for the individual’s general health care and providing referrals to specialists if necessary. There is generally no coverage outside the network. There are exceptions to using just doctors and medical facilities on the list during times of emergency, or when medically necessary (Health Insurance in-Depth).

Preferred Provider Organization

A PPO is similar to a HMO in that an individual pays a fixed monthly fee, and co-payments upon visits; however, the individual has more choices in provider selection. Unlike the HMO the PPO doesn’t require a “gatekeeper” physician to see a specialist. Should an individual want care outside of their network, the PPO plan generally covers expenses, but at a smaller percentage. An out of network visit usually requires a deductible. Bottom line is that a PPO gives individuals more choice, which many view as better service, and as a result is the most expensive Managed Care plan. PPOs are also the most popular form of Managed Care (Health Insurance In-Depth).

Point Of Service

Point of Service (POS) medical care limits choice, but offers lower costs when compared to HMOs and PPOs. Generally an individual chooses a primary health care physician within a health care network. The physician becomes “point of service”. An individual’s primary health care physician can refer the individual outside of the network, but with limited cost coverage. Interestingly, POS requires that an individual do their own paperwork if seeking care outside of his/her network; individuals must fill out forms and keep track of receipts (Health Insurance In-Depth).

Medical Savings Account

Medical Savings Accounts are not common so the description of this medical care plan will be brief. Medical Savings Accounts (MSA) can only be offered by employers with 50 or less employees. The employee welfare policy must follow strict government guidelines. Tax deductible monies are deposited on a periodic basis in a MSA at costs lower then other programs. The trade-off for the lower cost of the program is a higher deductible should medical care be needed, perhaps for an emergency. Financial requirements apply as listed in government guidelines, as well. Deductible limits are $1,650 - $2,500 for an individual and $3,300 - $4,950 for a family. If an MSA sounds like it might be the right way to go, get more information at healthinsuranceindepth.com.

Dental Care

Dental care insurance is not the main focus, but is certainly worth mentioning. Individuals enrolled in Dental Insurance Plans pay a monthly premium for coverage. Generally the higher the dollar figure, the better the coverage. Sometimes an individual medical coverage may cover dental; however, this is not usually the case. There are two main types of dental plans. One is called the traditional care plan; the other is referred to as Managed Dental Care. Generally basic dental costs, such as visits and cleaning, are covered under both plans. Managed Dental Care works much like a PPO; individuals can choose a primary dentist (much like a primary physician) from a list of select locations only. Premiums are lower then traditional care, but choices are minimal (Health Insurance In-Depth). For more information see the web-links section for Dental Insurance carriers with descriptions that is attached to the document.

Vision Care

Many vision service providers offer a managed care approach to vision care as opposed to the traditional fee-for-service plan. Group plans that can bring down costs significantly are affordable and beneficial to all. The goal for the employer is to find the best quality plan at a reasonable cost, with employee satisfaction as the number one priority. “With an employer paid managed care plan, the employer pays a set monthly rate per enrolled employee (including spouse or family). This allows an enrollee to receive, within the plan guidelines, an exam, frame, and lenses at no cost to them” (SVS).

Advantages and Disadvantages

Advantages and disadvantages of HMO health insurance

Many people enjoy having an HMO as health

insurance because the plan does not require claim forms to see a doctor or

during hospital stays. The HMO member only has to present a card that states

proof of insurance at the doctor's office or hospital. In an HMO the members may

have to wait longer for an appointment than with an indemnity insurance plan.

The HMO charges a fixed monthly fee so its members can receive health care.

There will be a small co-payment for each doctor visit; however with the HMO,

fees can be forecasted unlike a fee-for-service insurance plan. Although

freedom of choice is given up, out-of-pocket expenses are very low. In an HMO

there are some disadvantages. The premium that is paid is just enough to cover

the costs of doctors in the network. The members are “stuck” to a primary care

physician and if managed care plans change, then the member may not be able to

continue with the same PCP. On major disadvantage is that it is difficult to

get any specialized care because the members must get a referral first. Any

kind of care that is sought that is not a referral or an emergency is not

covered. The HMO plan is one of the fastest growing types of managed care in

terms of expenses, while being the most restrictive type of health care.

Advantages and disadvantages of PPO

insurance

As a member of a PPO, health care costs are low when the member stays within the provided network. This plan allows more freedom than an HMO in many ways. The member is not required to choose a primary care physician and can see a specialist without a referral, including the specialists that are outside the network. If care is sought outside the network the costs are more expensive and all of the paperwork can be the individual’s responsibility. This plan offers a large network to choose from and an array of doctors. Co-payments will be more expensive than other types of managed care due to the cost of extra amenities provided. PPOs are less expensive than a fee-for-service type. There are no deductibles in most plans; however, in some cases the member may need to pay one before receiving care. The out-of-pocket costs are large and the plan is limited in some ways, such as having to stay in the main network of doctors and specialists.

Advantages and disadvantages of POS insurance

A POS type of plan acts like an HMO except that it has more freedom when it comes to choosing doctors and facilities. This type of plan allow for its members to travel outside the network at a higher deductible. The plan uses preventive care, as it is more cost effective in the long run. The member has to pay a small amount of co-insurance, if any at all. Regular office visits require small co-pays. If the member wants to travel outside the network it must first meet the deductible requirement and then pay a percentage of the expenses. The premiums are more expensive than an HMO but allow more freedom.

Advantages and disadvantages of MSA insurance

An MSA plan is good for a small business because the premiums are more affordable. Instead of having a policy with high premiums and low co-pays the MSA offers a high deductible in case of an emergency or a major medical expense. The member has complete control over doctor and facility selection. The MSA plan requires the member to make regular deposits into a medical savings account to cover minor expenses. The member has to be able to afford the bill before meeting the requirements for the deductible. All deductibles must be paid to in order to receive any kind of medical care. A disadvantage for large businesses is that this type of plan is not available. Deposits made toward the medical savings plan are one hundred percent tax-deductible, and can be used towards any out of pocket medical expenses. For example, deductibles and regular office visits would be paid using the MSA. This allows you to pay for healthcare expenses with pretax dollars, a great advantage. All of the money that is not used for medical expenses will stay in the account until needed. This plan is one of the most expensive plans giving the least amount of restrictions. Here is a link to a company that offers an MSA: www.msabank.com.

How to Choose the Right Plan

Self-Insurance

The first step in choosing health insurance is deciding whether to self-insure, purchase insurance through a Managed Care Provider, or some other source. Self-insurance requires an employer to “pay employees’ medical bills directly, employing a healthcare company to act as an administrator” and is generally known as the riskiest model on the market (Unkovic). If an employer chooses to self-insure, the employer must follow federal guidelines set by the Employee Retirement Income and Security Act of 1974 (ERISA). Self-Insured employers are exempt from state regulation according to ERISA as federal law is the supreme law of the land. Therefore, self-insured employers are exempt from state “reserve requirements, mandated benefits, premium taxes, and consumer protection regulations” (Kaiser). States impose heavy regulation and taxation on insurance companies, but are not allowed to do the same with federal plans. As a result, federally regulated self-insurance medical plans are generally less expensive then state regulated plans; however, there is more risk exposure.

Say fifty percent of employees from a large company catch a highly contagious strain of spinal meningitis and must be hospitalized. The net result could be detrimental to the company, perhaps even causing insolvency. To avoid catastrophic loss, some companies will self-insure up to a certain amount, and will purchase excess insurance to cover amount beyond what is retained. This can be viewed as a large aggregate deductible of sorts where after the retained amount is met, the excess insurance comes into effect. Excess insurance is a good form of self-insurance insurance, also known as a stop-loss policy, which is relatively affordable.

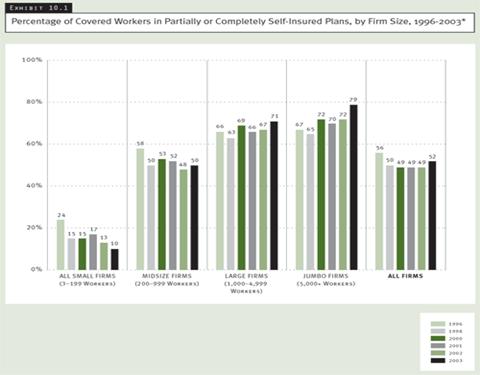

Self-insurance plans are fairly popular. In 2003, 52 percent of insured employees were enrolled in a plan that was completely or partially self-insured (Kaiser). Self-insurance is better suited to larger firms then smaller because of its inherent risk. Spreading the risk over a large number of employees is more economically viable then spreading risk over a few employees; smaller companies likely do not have the financial resources to overcome a catastrophic medical event. According to the Henry J. Kaiser Foundation Family, “The likelihood that an employer self-insures is highly related to the size of the firm. Ten percent of covered workers in all small firms (3 to 199 workers) are in self-insured plans, compared to 50% of workers in mid-size firms (200-999 workers) and 79% of workers in jumbo firms (5,000 or more workers)”- see Exhibit 10.1 next page.

Like most government regulated plans, self-insurance guidelines can be confusing. It is recommended that one talk with an attorney that specializes in ERISA law associated with self-insurance before taking the plunge in this direction. Also, because of strict ERISA guidelines, employers generally contract with a Third Party Administrator (TPA) or an insurance company to act as one. TPAs generally collect premiums, pay claims, and handle other paperwork such as the annual Summary Plan Description or SPD (Ohio Department of Insurance).

The decision to self-insure or purchase insurance must be based on an evaluation of the comparative costs and benefits associated with each. Comparative risk might cause a smaller company to purchase insurance to avoid potential insolvency, even though to self-insure could have lower costs in the short run. A larger company may have enough employees and enough capital to effectively spread the risk of a potential catastrophic event, and choose self-insurance thereby minimizing costs.

http://www.kff.org/insurance/ehbs2003-12-chart.cfm

Purchasing from a provider

Group health insurance provides insurance for a large number of employees, dependents, or retirees. Eligible people are covered in spite of their age or physical condition. In general, group health insurance is provided by employers, professional and trade organizations, unions, social or political groups, and governments.

Small group health insurance applies to businesses with a small number of employees, sometimes one or two employees, but usually between three and twenty-five. As many as one hundred employees may qualify for small group health insurance. Prices on small group health insurance are determined based on two criteria: the expenses of medical services are in a restrictive area and small group health insurance is in a planned operation of services.

Advantages of purchasing from a provider

Providing health care coverage helps attract and retain competent employees. Even if employers require employees to pay their own premiums, the rate is usually lower than that of an individual plan and can be deducted from a tax-free medical expense account established by the employee. The employees also benefit by not having to physically qualify for the coverage. The main reason for an employer to purchase group health insurance is self-preservation; because providing health care benefits is conventional and expected, competent employees will seek employment elsewhere or demand a higher wage to offset their insurance premiums if their employer does not provide health insurance. High job turnover and position vacancy are extremely expensive to businesses in terms of lost work capacity. Additionally, the insurance premiums are tax deductible for the business and the benefits can be viewed as additional, untaxed income for employees. Providing benefits also improves corporate efficiency because the employees tend to be happier and healthier and have higher work productivity.

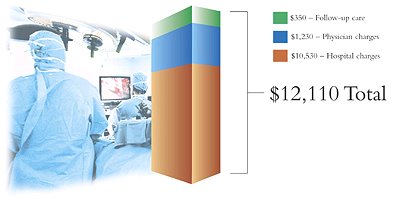

Health coverage also protects against the high financial exposure that may accompany even common accidents or illnesses. Consider what the cost of a typical hospital stay may be (3 days and 2 follow-up visits): **Figures are for illustration purpose only. Actual costs may vary. (Why)

In general, small group health insurance is more reasonably priced than individual plans. It is less expensive because fixed costs are distributed over a larger number of policies. Premiums are even lower for large group health insurance.

Small business health insurance allows the “spread of financial risk between all the members,” which enables members to simultaneously pay lower premiums and expand plan coverage for employees.

Small business health insurance is applicable as long as the employer has two or more full-time, taxable employees (www.healthins.indepth.com).

Disadvantages of purchasing from a provider

In 1997, a survey by the American Health Care Association revealed that less than 6 percent of eligible employees buy group long-term health care insurance. The reason for the low rate of group health insurance participation is the “adverse selection,” which means that the majority of the people who sign up for health insurance have pre-existing health problems and file numerous claims. As a result, group long-term care insurance companies raise rates relative to individual plan rates to cover the higher group claim rates and payments.

Purchasing insurance from a provider can be costly due to high overhead: “printed literature, pay company sales representatives, provide enrollers, maintain help phone lines, provide service personnel to handle problems and maintain a claims department.” Lower net income (premiums minus claim payments) results in an increased percent paying the fixed overhead costs. The effect of the group policy is a smaller benefit than for individual plans at the same cost. Large group premiums are normally between 30 percent and 100 percent higher than individual coverage (Day).

Small businesses are also disadvantaged in purchasing from a provider because health care premiums are lower if the business is paying for more employees.

One of the main disadvantages of group health insurance is the restriction of plan choices for employee selection, i.e., if a company offers only an HMO program, employees have no choice but to take what is offered.

Guidelines

The local chamber of commerce can provide information about community group insurance purchasing pools. State insurance departments are another source for finding an insurance provider (Strength).

This information, compiled by the Institute for Health Policy Solutions, is current as of April 2001. It focuses on groups that offer recipients a choice of health plans.

|

State |

Plan |

Size of Firm |

Region |

Phone Number |

|

California |

Pacific Health Advantage |

2-50 employees, or employers of any size if they obtain coverage through a qualifying trade association. |

Statewide |

(949) 766-1905 |

(Strength)

Employers should consider using a state-licensed broker for group health insurance purchases. Brokers can guide employers in finding suitable group health insurance for their employees. Registered Health Underwriters are brokers who have completed required coursework and passed exams dealing with the health insurance industry.

Needs and Wants of Employees

Some health plans offer a network of doctors. If employees have personal family doctors they wish to keep, additional costs might be incurred to accommodate these preferences, or visits to these doctors might not be covered at all.

Some health plans will not allow you to go out of network for coverage, meaning that employees must pay completely out-of-pocket for being seen by a doctor that is not on a given list of providers. However, out of network coverage can usually be added at a cost.

Preventive services vary for each provider; adequate check-up exams should be included in desirable insurance plans.

Prescription drug benefits are very important for employees; the prescriptions that are and are not covered vary by provider and plan choice. Employers should try to provide the maximum benefit to employees by selecting a plan that will provide prescription benefits the majority of employees.

Cost of group health insurance for employees is always a big concern. Higher co-payments decrease employee premiums. Co-payments are a form of cost-sharing that require insured people to pay a fixed dollar amount for a received medical service. Increase deductibles are another way to lower employee out-of-pocket costs. Deductibles are a fixed dollar amount which an insured person pays before the insurer starts to make payments for covered medical services during the benefit period, usually a year (Group).

Requirements for Employers

Requirements differ by the various health care insurance providers. In order to qualify for a group plan such as Athem, the employer of the company must provide a copy of the state and federal tax form to show proof of his/her legal business, home-based employers must show proof of working at least 30 hours per week at his/her business, and employers must provide evidence of running a business for three consecutive months (http://moneycentral.msn.com).

Requirement for Insurers

Insurers are required to check that the members of the company who are purchasing health insurance actually work for the employers. In addition, various documents are essential for sole proprietors to provide to the insurer or health plan administrator on a yearly basis. Deciding how to implement a medical benefits program is not as easy as understanding the similarities, differences, advantages, and disadvantages of each type, there are many other challenges facing employers and employees with regards to medical care packages.

Challenges Concerning Medical Benefits

Rising Costs

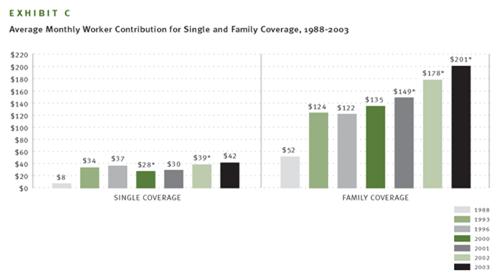

According to the Washington Post, “Employer health care costs rose 12 percent in the past year (2003), on top of a 16 percent increase the previous year (2002), according to Towers, Perrin, Forster & Crosby Inc., a human resources consulting firm” (Downey). This rise in costs is affecting many aspects of business and even consumers. For example, with every mid-size car DaimlerChrysler builds in the US, it will cost an additional $1,300 for employee health care (Downey). This will surely put a damper on sales. In 2001, the average amount paid for medical benefits by employers was $5,266 per employee (FisherVista). The average amount a family spent on healthcare in 2003 was $756 per month ($9,072 per year) with employers picking up $555 ($6,660 per year) of the tab (Kaiser). The average worker contribution for family coverage has gone from $52 in 1998 to $201 in 2003 (Kaiser).

http://www.kff.org/insurance/ehbs2003-12-chart.cfm

The debate rages over reasons why Managed Care costs are rising. According to the National Center for Policy Analysis (NCPA), “a primary reason health care costs are soaring is that most of the time when we enter the medical marketplace as patients, we are spending someone else’s money” (Herrick). The NCPA explains, “Economic studies and common sense confirm that we are less likely to be prudent, careful consumers if someone else is paying the bill. When we are paying our own medical bills, we are conservative consumers (Herrick).”

Experts at The Henry J. Kaiser Family Foundation hold a different view. They attribute cost problems to advances in medical technology, including prescription drugs, as the biggest reason health care costs are rising (Kaiser).

In yet another view, many critics of the current medical insurance program say that the reason for such dramatic increases in premiums is due to the greedy insurance industry. According to California Senators Figueroa and Burton, and Assemblyman Laird:

HMOs and health plans claim that skyrocketing premiums are the result of increasing medical costs. However, in 2002, the cost of health insurance for a family of four increased 250% more than the rate of medical inflation. According to a report by the Standard & Poor's managed care analyst, Phillip Seligman, HMOs and health plans should continue to reap record profits fueled by premium price hikes in the 15% to 18% range. Premiums are expected to continue to outpace medical-cost inflation in 2003 (Calhealthconsensus.org).

There are those who claim that the uninsured are the reason costs are on the rise. Under current law, medical facilities legally cannot turn away individuals in need of necessary care. Medical facilities in the past have tried numerous methods of collection for non-payment of services. Recently, however, hospitals and medical facilities have been harassed by the Department of Health and Human Services for aggressive collection tactics. If uninsured individuals are not required to pay, then those who are paying their bills pick up the tab. This results in either higher premiums or the government subsidizes medical facilities resulting in higher taxes. According to the Detroit News, an aging population is a factor in the rise of costs. As individuals get older, their medical needs and/or expenses rise. As a result, the costs of medical care for all increases.

It is not difficult to see how rising costs affect an economy. If an employer foots the bill for the rising costs of medical benefits, it means lower wages for employees and/or fewer employees. If employees foot the bill, they will have less disposable income to spend, which, once again, will put less money into the non-healthcare economy. Bottom line, rising costs prevent money from entering the non-healthcare economy, translating into fewer businesses, fewer jobs, a weakened economy, and a lower standard of living.

Changes in Legislation

Changes in Legislation can be costly, and if not followed to the letter of the law even more so. California bill SB-2 is a good example of how confusing legislation can be, and how changes in legislation can affect Managed Care with respect to employers. SB-2 will require most employers with 20 employees or more to pay a fee to cover the cost of a state health care plan. If the employer provides the health care, the employer receives a credit to offset a percentage of the fee. If an employer does not comply with SB-2, there is a penalty fee imposed of 200% of the original mandated fee (Burton). Following legislation to the letter of the law is of the utmost importance; a TPA or a risk management expert is highly recommended when dealing with legislation to ensure that it is dealt with accurately. According to the Employment Policies Institute, SB-2 titled the Health Insurance Act of 2003 will cost California employers $11.4 billion annually. Logically this will affect jobs: “Employees are at risk of losing their jobs, either through labor force cuts or competition from more experienced workers attracted by the new benefits. Either way, the least skilled workers could find themselves out of the labor force” (Yelowitz).

On the flip side, assuming something positive is coming from Managed Care or any legislation for that matter, a tax break for employers offering Health Benefits for example, can take years to implement. According to Republican Fiscal Staffer, Therese Tran, a bill takes an average of 2-3 years to be implemented. A bill introduced on either the Senate or Assembly floor must go through quite a process. First it goes to a Policy Committee. If there is a cost or “fiscal impact” (Tran), the bill goes to an Appropriation Committee, then proceeds to the floor of that house for vote. If passed, the bill continues to the second house and is run through the same process. If there are no changes, then it is adopted and is sent to the governor for signing. If the bill has been changed, it goes back to the house of origin for “concurrence” (Tran)—this can go back and forth. Therefore, if a new tax break or statute is going to benefit businesses, it is likely that companies will have to wait a couple of years for it. In the mean time, here are other possible solutions that can be implemented right away.

Solutions to Rising Costs

One of the proposed solutions to rising costs deals directly with the concept that people will spend more when someone else is paying for it. Higher co-pays have been proposed for traditional Managed Care Plans such as HMOs, PPOs, etc, as a deterrent against wasteful medical usage. Wasteful medical usage causes indirect price inflation for everybody within his or her respective self-insurance, or insurance pool. Remember what the National Center for Policy Analysis says, “When we are paying our own medical bills, we are conservative consumers” (Herrick). When individuals are required to pay a more substantial portion of their medical bills such as a higher co-pay, the thought is that that person will be more conservative and spend less time on frivolous issues. Also supporting this view, a survey was conducted by Watson Wyatt-NBGH that included 449 employers (accounting for eight million employees). Its findings provided that the highest performers, those with lower than seven percent increases in health benefits last year, “reported adding financial tension in their plans through increasing premiums, raising costs at the point of care, or implementing a high-deductible health plan without a reimbursement arrangement. They also provided information and tools to help employees make better purchasing decisions” (Carlson and Elswick).

To address the Kaiser view, which attributes cost problems to “medical technology” and the “costs of prescription drugs”, a greater emphasis on using cheaper generic drugs rather than the expensive and unnecessary brand name drugs, could significantly cut costs (Warden). This could be also be accomplished by allowing importation of prescription drugs. Senator John McCain espouses this belief stating importation is “another lost opportunity for cost containment.” He claims, “Americans spend hundreds of millions of dollars on imported pharmaceuticals – not because they don’t want to buy American, but because they simply can’t afford to (McCain).” Prescription drugs are much less expensive in Mexico, and other foreign nations. Mr. McCain wants America to have access to them, and feels Managed Care costs could be cut way down if America contracts with foreign companies. Those who oppose importations of inexpensive prescription drugs claim that there is no way of ensuring their quality. In a free market, a company’s reputation will determine its demand; thus, choice should be in the hands of the people, especially when it makes economic sense. To assume that the only country is capable of quality prescription drugs is the United States is naive. Generic and importation of prescription drugs will also help curb the effects of the largest consumer group, an aging baby boomer population.

Solutions by way of Legislation

There are numerous ways in which changes achieved through legislative means can be helpful to both employers and employees. Limiting the states ability to levy taxes and charge fees to a certain percentage would allow businesses and/or employees to better afford health care. Overtaxation of employers raises costs and kills businesses. Without businesses there are no jobs, and without jobs we have no economy. Businesses must be protected.

A cap on the amount of state legislation looked at per year (with federal government extension grants), would force legislators to budget time more efficiently. This would force the government to operate more like a business and focus on issues that matter such as Worker’s Comp, Managed Care, etc.

A solution to the problem of medical treatment of the uninsured is difficult to muster. On one side the spectrum, is to require individuals who have used medical services to pay the facilities back. On the other side, instituting a socialized medical plan for all can eliminate the uninsured status of individuals. Another solution to the problem could relate to the aforementioned limit of state taxation. By lowering taxes, perhaps companies would be able to operate at higher margins and be better able to fund employee’s health care.

In addition to the SB-2 proposal, which may take effect as early as January 2006 (calhealthconsensus.org), there are many other bills in the works in the California legislation. Some are further along in the process than others. Each bill has unique characteristics that have both positive and negative impacts. It will be interesting to see how things begin to take shape in the next few years. Here is a short description of each of the new laws provided by CalHealthConsensus.org:

AB 1960: Improving

Transparency within the Drug Purchasing Process

Pharmacy benefit managers (PBMs)

are fiscal intermediaries that specialize in the administration and management

of prescription benefit programs for clients such as state governments, HMOs,

employers, and union trust funds. Currently, PBMs have no fiduciary duty to

their clients, and often do not disclose the true cost of drugs they are

providing for their clients or the discounts, kickbacks or rebates they receive

from drug manufacturers.

SB 1144: Prescription

Drug Reimportation

Directs the state Department of General Services

to bulk purchase drugs for four state agencies (Department of Corrections,

Department of the Youth Authority, Department of Developmental Services,

Department of Mental Health) from Canada. U.S. Made prescription drugs are

available in Canada at savings of 30%-60%.

SB 1349: Health Insurance

Rate Oversight

Requires health insurance companies to get

approval for rate increases from the Department of Insurance. The approval

process would require health insurance to justify their administrative costs,

overhead, executive salaries, and profits. The Insurance Commission would have

authority to deny rates deemed unfair or excessive. 26 states have some form of

health insurance premium oversight. As of yet, California has no such review

process.

AB 1958: Prescription

Drug Purchasing Pool

Expands California's purchasing power by

authorizing the California Public Employees\' Retirement System (CalPERS) to

form a purchasing pool for prescription drugs for public and private purchasers.

Allows other California institutional purchasers of prescription drugs, such as

businesses and HMOs, to join the pool and take advantage of the state's

purchasing power to achieve lower prices.

SB 2: Employment Based

Health Care Coverage

The purpose of SB 2 is to assure that all

workers and their families have health coverage by requiring employers either to

purchase that coverage or pay a fee to a state fund that will purchase coverage

for workers and their families.

SB 26: Health Insurance

Cost Control Legislation

California's 6.2 million

uninsured population is projected to grow over the next 10 years unless the

state acts to control costs. SB 26 will require health insurers to prove to

state regulators that rates are not unfair or excessive.

SB 921: The Health Care

for All Californians Act

The Health Care for All

Californians Act would provide health insurance coverage to all Californians

through a single insurance plan offered by the State of California.

Relationship to the Employee Benefits Wheel

There are many influences that affect the medical benefits offered at any given company; these can be described and analyzed by means of the employee benefits wheel.

External Factors

Competition- Managed health care is provided on the basis that employers would like to attract and retain employees. The external factor of how other firms are providing health care benefits compared to one’s own company is a direct reflection of how competitive one wants to be in attracting and retaining employees. Competition can control the types of managed care provided by one’s business.

Inflation- This is an external factor that is one of the largest contributing factors to how much and what type of managed health care a company can provide. Due to inflation in the cost of medical insurance premiums, not the procedures, as well as, the cost of prescription drugs, the cost of medical insurance has increased dramatically each year. This is an external factor that can put a company out of business no matter what the competition is doing or what laws are put into place. If a company does not have the financial stability to pay for these costs then it will be put out of business. Likewise, these costs can hamper the ability to attract and retain competent employees; therefore, it will be driven out of business in a different way.

Legal Requirements- as stated earlier, law provides some requirements for insurance. SB-2 is a legal requirement that will make employers provide medical insurance to all or contribute to a fund that will provide medical insurance for employees. Businesses have no control over legislation once its been passed. SB-2 may cause companies to relocate outside of California in order to be able to do business and still be competitive in the market.

Taxation- Managed health care plans provide tax advantages to employees. If an employee must pay for his/her own health insurance or if he/she partially pays for coverage, and the business provides the health coverage, then the coverage is paid for using pre taxed dollars. If the company does not provide health coverage insurance, then the employer may provide flexible spending accounts where some monies go toward health coverage insurance. The graph below shows an example of how an employer can save about $675 dollars for the employee that makes $45,000 a year with a flexible spending account.

|

|

Using flexible spending accounts |

Not using flexible spending accounts |

|

Combined income |

$45,000 |

$45,000 |

|

Health care expenses |

( 1,000) |

0 |

|

Dependent care expenses |

( 3,500) |

0 |

|

Taxable income |

40,500 |

45,000 |

|

Federal income and Social Security taxes |

( 6,075) |

( 6,750) |

|

Take home pay |

34,425 |

38,250 |

|

Health care expenses |

0 |

( 1,000) |

|

Dependent care expenses |

0 |

( 3,500) |

|

Spendable pay |

$34,425 |

$33,750 |

|

Tax savings |

$675 |

|

Benefit Innovation- The benefits “industry” is in constant change as new ideas and “perks” and included in compensation packages. There are always new ways to provide something unique. The main purpose of benefit innovation in managed health care is to provide great service at a lower cost to both the employer and the employee. One type of benefit innovation for managed health care was recently implemented in January 2004. It is the Health Savings Account (HSA). It differs from an MSA because it allows an employee to move from job to job and it rolls over every year. The concept of allowing an employee to change jobs freely is not a way to retain, but possible changes in laws like SB-2, makes saving money more important so that you can pay your employees more. If every business has to provide medical insurance, then it will be more important to provide a higher total compensation strategy.

Internal Factors

In addition to the many external factors that influence employee medical benefits, there are also five internal factors that play a role.

Total Compensation Strategies- Managed health care was first put into place by businesses to attract and retain employees through use of a total compensation strategy. TCS is the total of the wages plus the benefits. Since health care benefit costs are so high, employers that can provide good packages to their employees are providing a better TCS than those companies that pass along the cost to there employees. The cost is either passed on through lower wages, fewer positions available, or transference of the cost, making the employees pay for the benefits themselves.

Wants versus Needs- When dealing with managed health care, the wants and needs are fairly simple. The question is not: do the employees want health insurance or do they need it. The big question for the employer is do we want to pay for it or do we need to pay for it? In order to figure this out you can survey the employees and see how they feel about different total compensation strategies. This is an effective way to find out if employees know the value they are receiving from the managed health care plan, if you are even providing one.

Cost Issues- The increasing costs of health insurance plagues everyone daily. Higher costs for insurance causes lower wage increases. In a study done in Wisconsin, if insurance increases at a rate of 11.04 % annually and a salary for teachers with a BA increases at 3.07 %, by 2014-2015 insurance will be 100.15% of the teacher’s salary (Wasb). In order to lower costs for the teachers’ insurance, a managed care plan will be adopted. This will allow increases in wages, as well as, provide medical insurance. Cost issues can be quite tricky because without profits, the business does not survive, and without benefits there are no employees to run the business. There is a fine line between what a company “wants” to afford and what is can and should afford.

HR Management Philosophy- This is the underlying philosophy of an individual company. It is established at the beginning of the companies’ creation. This philosophy; however, may morph and change as new laws are implemented, costs change, new management presides in top positions, and/or new plans evolve. For example, some businesses hold a progressive view and believe that everyone should have adequate medical insurance. If the company wants to provide medical coverage to retired employees, then it will find a way to provide it no matter what the costs. This philosophy is like the conscience of the company. Some companies have a conscience while others do not, just like people.

Business Objectives- The business objectives of a company usually outline goals for the future of the company; however, they can change. Businesses can be in various stages of life—growth, stabilization, maturity, or decline. Because positions can change over time, objectives can change as well. If a company is involved in an acquisition, it must decide how it wants to incorporate the acquired employees into the current medical plan, or if a new plan will be structured. On the flip side, if a company must layoff workers, there may be a need to restructure the current health benefits and a “take-back” situation may occur.

In the realm of medical benefits and managed care plans there are no easy answers. Each type of plan presents an employer with both advantages and disadvantages. In addition, there are many factors to consider and problems to overcome. Legislation in the medical insurance realm is now becoming a reality—transferring it from a benefit into a mandated social insurance program. Is this really a good idea?

Web Links

This section provides brief summaries for key web sites:

A website for those who wish to manage health care on their own. A Voltaire quote from the HealthWorld home page sums up their philosophy, “The art of medicine consists of amusing the patient while nature cures the disease.”

The American Journal of Managed Care - http://www.ajmc.com

A very thorough and technical view into Modern Managed Care and Theoretical Managed Care for the Future. Information ranges from idealistic to realistic vision. The AJMC considers itself “The Forum for Peer-Reviewed Literature on Health-Care outcomes.”

The Department of Managed Care - http://www.hmohelp.ca.gov

A comprehensive Californian government website displaying: Information about Health Plans, a California HMO report card, Press Highlights, Regulations, and many other Managed Care topics.

Glossary of Terms in Managed Health Care - http://www.pohly.com/terms.html

According to their own description, this glossary has ‘hundreds of terms with definitions; a helpful resource for those working in health and medical fields striving to understand new managed care terminology.”

Dental Insurance Providers

From its home page; “Aetna is one of the nation's leading providers of health, dental, group, life, disability and long-term care benefits.”

Premier Access http://www.premierppo.com/

One of the largest dental PPO (Preferred Provider) networks in California created by a group of dentists who are experts in the field.

Vision Insurance Providers

Eye and Vision Insurance - http://www.fritzmondale.org/eye_and_vision_insurance.html

An insurance broker with access to different insurance companies.

VSP - http://www.vsp.com/

From it website: “At VSP, we’re dedicated to offering affordable, high-quality eyecare plans that put people first, support visual wellness and improve one’s quality of life. As the nation’s largest provider of exceptional eyecare coverage, more than one in 10 Americans rely on VSP for eyecare wellness.”

Works Cited

Burton, John. Senate Bill-2 Chaptered October 6, 2003. Date Accessed April 16, 2004.

http://info.sen.ca.gov/pub/bill/sen/sb_0001-0050/sb_2_bill_20031006_chaptered.html

California Department of Insurance (Revised July 2003). Health Insurance

Downey, Kirstin. A Heftier Dose To Swallow: Rising Cost of Health Care in U.S. Gives Other Developed Countries an Edge in Keeping Jobs. Washington Post, Saturday, March 6, 2004.

California Health Consensus website: Working Together for Universal Health Care Solutions. Retrieved March 5, 2004 and April 18, 2004 from http://www.calhealthconsensus.org

Carlson, Leah and Elswick, Jill. Employers Adopt Aggressive Health Benefit Plan Designs. Employee Benefit News, April 15, 2004. Retrieved on April 19, 2004 from http://www.benefitnews.com/health/detail.cfm?id=5820.

Day, Thomas. “Finding the Right Purchase Source, Product and Company

www.longtermcarelink.net/find_insurance_source.html

Fisher Vista Website: Marketing Services for the Human Capital Industry. Retrieved on March 1, 2004 from http://www.fishervista.com/statistics.htm

Group and Individual Health Plans

www.csba.com/member_benefits/Grouplndi.html

Group Health Insurance (Purchasing Group Health Insurance)

www.insureants.com/Group_Health_Insurance.htm

Health Insurance In-Depth. Date Accessed March 3, 2004. http://www.healthinsuranceindepth.com

Herrick, Devon. Why Are Health Costs Rising? Brief Analysis No. 437. National Center for Policy Analysis, Wednesday, May 7, 2003. Date Accessed April 14, 2004.

http://www.ncpa.org/pub/ba/ba437/

Kaiser editors et. all. Employer Health Benefits 2003 Annual Survey. The Henry J. Kaiser Family Foundation. Date Accessed April 15, 2004.

http://headlines.kff.org/healthpollreport/templates/summary.php?feature=feature5

McCain, John. Statement of Senator John Mccain on the Medicare Conference Report, Monday, Nov 24, 2003. Date Accessed April16, 2004.

http://mccain.senate.gov/index.cfm?fuseaction=NewsCenter.ViewPressRelease&Content_id=1192

Merrium-Webster (m-w).

http://www.m-w.com/cgi-bin/dictionary?book=Dictionary&va=budget

MSN Money. Retrieved from http://moneycentral.msn.com

Ohio Dept of Insurance Self-insured employers.

Date Accessed April 15, 2004.

http://www.ohioinsurance.gov/consumserv/scripts/pubdisp.asp?pubtype=HEALTH&pageseqnum=10

SVS Vision. Group Discount Plan, 2000. Date Accessed April 18, 2004. http://www.svsvision.com/v_group.asp

State of California, Office of the Patient Advocate. Date Accessed March 27, 2004.

http://www.opa.ca.gov/report_card/report/group.asp?report_group=med-groups

Tran, Therese. Republican Fiscal Staffer. Personal Interview. March 26, 2004.

Unkovic, Alexis. Buying Health Insurance, October 2003. SMC Business Councils.

Date Accessed April 14, 2004. http://www.smc.org/Article.cfm?id=242

Warden, Gail. Solutions exist to cut medical costs, Tuesday June 11, 2002.

Date Accessed April 18, 2004.

http://www.detnews.com/2002/editorial/0206/11/a07-511376.htm

Wisconsin Association of School Boards website. Date Accessed April 20, 2004. http://www.wasb.org/employee/02insurance.pdf

Why Purchase Group Health Insurance

http://isg.unicare.com/maj_bu/small_group/virginia/Flex_Why.htm

Yee, Leland. Assembly Concurrent Resolution (ACR) No. 144—Relative to Feng Shui.

http://info.sen.ca.gov/pub/bill/asm/ab_0101-0150/acr_144_bill_20040304_amended_asm.html

Yelowitz, Dr.

Aaron.

The Cost of California's

Health Insurance Act of 2003.

Employment Policies Institute, 2003. Date Accessed April 15, 2004.

http://www.epionline.org/study_detail.cfm?sid=67