Managed Care Introduction -- Managed Care Types -- Advantages and Disadvantages -- How to Choose the Right Plan

Challenges Concerning Medical Benefits -- Relationships to Employee Benefit Wheel -- Web Links Page -- Works Cited

Challenges Concerning Medical Benefits

Rising Costs

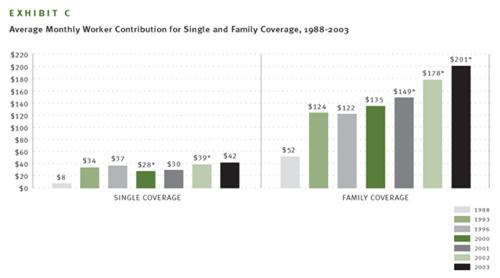

According to the Washington Post, “Employer health care costs rose 12 percent in the past year (2003), on top of a 16 percent increase the previous year (2002), according to Towers, Perrin, Forster & Crosby Inc., a human resources consulting firm” (Downey). This rise in costs is affecting many aspects of business and even consumers. For example, with every mid-size car DaimlerChrysler builds in the US, it will cost an additional $1,300 for employee health care (Downey). This will surely put a damper on sales. In 2001, the average amount paid for medical benefits by employers was $5,266 per employee (FisherVista). The average amount a family spent on healthcare in 2003 was $756 per month ($9,072 per year) with employers picking up $555 ($6,660 per year) of the tab (Kaiser). The average worker contribution for family coverage has gone from $52 in 1998 to $201 in 2003 (Kaiser).

http://www.kff.org/insurance/ehbs2003-12-chart.cfm

The debate rages over reasons why Managed Care costs are rising. According to the National Center for Policy Analysis (NCPA), “a primary reason health care costs are soaring is that most of the time when we enter the medical marketplace as patients, we are spending someone else’s money” (Herrick). The NCPA explains, “Economic studies and common sense confirm that we are less likely to be prudent, careful consumers if someone else is paying the bill. When we are paying our own medical bills, we are conservative consumers (Herrick).”

Experts at The Henry J. Kaiser Family Foundation hold a different view. They attribute cost problems to advances in medical technology, including prescription drugs, as the biggest reason health care costs are rising (Kaiser).

In yet another view, many critics of the current medical insurance program say that the reason for such dramatic increases in premiums is due to the greedy insurance industry. According to California Senators Figueroa and Burton, and Assemblyman Laird:

HMOs and health plans claim that skyrocketing premiums are the result of increasing medical costs. However, in 2002, the cost of health insurance for a family of four increased 250% more than the rate of medical inflation. According to a report by the Standard & Poor's managed care analyst, Phillip Seligman, HMOs and health plans should continue to reap record profits fueled by premium price hikes in the 15% to 18% range. Premiums are expected to continue to outpace medical-cost inflation in 2003 (Calhealthconsensus.org).

There are those who claim that the uninsured are the reason costs are on the rise. Under current law, medical facilities legally cannot turn away individuals in need of necessary care. Medical facilities in the past have tried numerous methods of collection for non-payment of services. Recently, however, hospitals and medical facilities have been harassed by the Department of Health and Human Services for aggressive collection tactics. If uninsured individuals are not required to pay, then those who are paying their bills pick up the tab. This results in either higher premiums or the government subsidizes medical facilities resulting in higher taxes. According to the Detroit News, an aging population is a factor in the rise of costs. As individuals get older, their medical needs and/or expenses rise. As a result, the costs of medical care for all increases.

It is not difficult to see how rising costs affect an economy. If an employer foots the bill for the rising costs of medical benefits, it means lower wages for employees and/or fewer employees. If employees foot the bill, they will have less disposable income to spend, which, once again, will put less money into the non-healthcare economy. Bottom line, rising costs prevent money from entering the non-healthcare economy, translating into fewer businesses, fewer jobs, a weakened economy, and a lower standard of living.

Changes in Legislation

Changes in Legislation can be costly, and if not followed to the letter of the law even more so. California bill SB-2 is a good example of how confusing legislation can be, and how changes in legislation can affect Managed Care with respect to employers. SB-2 will require most employers with 20 employees or more to pay a fee to cover the cost of a state health care plan. If the employer provides the health care, the employer receives a credit to offset a percentage of the fee. If an employer does not comply with SB-2, there is a penalty fee imposed of 200% of the original mandated fee (Burton). Following legislation to the letter of the law is of the utmost importance; a TPA or a risk management expert is highly recommended when dealing with legislation to ensure that it is dealt with accurately. According to the Employment Policies Institute, SB-2 titled the Health Insurance Act of 2003 will cost California employers $11.4 billion annually. Logically this will affect jobs: “Employees are at risk of losing their jobs, either through labor force cuts or competition from more experienced workers attracted by the new benefits. Either way, the least skilled workers could find themselves out of the labor force” (Yelowitz).

On the flip side, assuming something positive is coming from Managed Care or any legislation for that matter, a tax break for employers offering Health Benefits for example, can take years to implement. According to Republican Fiscal Staffer, Therese Tran, a bill takes an average of 2-3 years to be implemented. A bill introduced on either the Senate or Assembly floor must go through quite a process. First it goes to a Policy Committee. If there is a cost or “fiscal impact” (Tran), the bill goes to an Appropriation Committee, then proceeds to the floor of that house for vote. If passed, the bill continues to the second house and is run through the same process. If there are no changes, then it is adopted and is sent to the governor for signing. If the bill has been changed, it goes back to the house of origin for “concurrence” (Tran)—this can go back and forth. Therefore, if a new tax break or statute is going to benefit businesses, it is likely that companies will have to wait a couple of years for it. In the mean time, here are other possible solutions that can be implemented right away.

Solutions to Rising Costs

One of the proposed solutions to rising costs deals directly with the concept that people will spend more when someone else is paying for it. Higher co-pays have been proposed for traditional Managed Care Plans such as HMOs, PPOs, etc, as a deterrent against wasteful medical usage. Wasteful medical usage causes indirect price inflation for everybody within his or her respective self-insurance, or insurance pool. Remember what the National Center for Policy Analysis says, “When we are paying our own medical bills, we are conservative consumers” (Herrick). When individuals are required to pay a more substantial portion of their medical bills such as a higher co-pay, the thought is that that person will be more conservative and spend less time on frivolous issues. Also supporting this view, a survey was conducted by Watson Wyatt-NBGH that included 449 employers (accounting for eight million employees). Its findings provided that the highest performers, those with lower than seven percent increases in health benefits last year, “reported adding financial tension in their plans through increasing premiums, raising costs at the point of care, or implementing a high-deductible health plan without a reimbursement arrangement. They also provided information and tools to help employees make better purchasing decisions” (Carlson and Elswick).

To address the Kaiser view, which attributes cost problems to “medical technology” and the “costs of prescription drugs”, a greater emphasis on using cheaper generic drugs rather than the expensive and unnecessary brand name drugs, could significantly cut costs (Warden). This could be also be accomplished by allowing importation of prescription drugs. Senator John McCain espouses this belief stating importation is “another lost opportunity for cost containment.” He claims, “Americans spend hundreds of millions of dollars on imported pharmaceuticals – not because they don’t want to buy American, but because they simply can’t afford to (McCain).” Prescription drugs are much less expensive in Mexico, and other foreign nations. Mr. McCain wants America to have access to them, and feels Managed Care costs could be cut way down if America contracts with foreign companies. Those who oppose importations of inexpensive prescription drugs claim that there is no way of ensuring their quality. In a free market, a company’s reputation will determine its demand; thus, choice should be in the hands of the people, especially when it makes economic sense. To assume that the only country is capable of quality prescription drugs is the United States is naive. Generic and importation of prescription drugs will also help curb the effects of the largest consumer group, an aging baby boomer population.

Solutions by way of Legislation

There are numerous ways in which changes achieved through legislative means can be helpful to both employers and employees. Limiting the states ability to levy taxes and charge fees to a certain percentage would allow businesses and/or employees to better afford health care. Overtaxation of employers raises costs and kills businesses. Without businesses there are no jobs, and without jobs we have no economy. Businesses must be protected.

A cap on the amount of state legislation looked at per year (with federal government extension grants), would force legislators to budget time more efficiently. This would force the government to operate more like a business and focus on issues that matter such as Worker’s Comp, Managed Care, etc.

A solution to the problem of medical treatment of the uninsured is difficult to muster. On one side the spectrum, is to require individuals who have used medical services to pay the facilities back. On the other side, instituting a socialized medical plan for all can eliminate the uninsured status of individuals. Another solution to the problem could relate to the aforementioned limit of state taxation. By lowering taxes, perhaps companies would be able to operate at higher margins and be better able to fund employee’s health care.

In addition to the SB-2 proposal, which may take effect as early as January 2006 (calhealthconsensus.org), there are many other bills in the works in the California legislation. Some are further along in the process than others. Each bill has unique characteristics that have both positive and negative impacts. It will be interesting to see how things begin to take shape in the next few years. Here is a short description of each of the new laws provided by CalHealthConsensus.org:

AB 1960: Improving

Transparency within the Drug Purchasing Process

Pharmacy benefit managers (PBMs)

are fiscal intermediaries that specialize in the administration and management

of prescription benefit programs for clients such as state governments, HMOs,

employers, and union trust funds. Currently, PBMs have no fiduciary duty to

their clients, and often do not disclose the true cost of drugs they are

providing for their clients or the discounts, kickbacks or rebates they receive

from drug manufacturers.

SB 1144: Prescription

Drug Reimportation

Directs the state Department of General Services

to bulk purchase drugs for four state agencies (Department of Corrections,

Department of the Youth Authority, Department of Developmental Services,

Department of Mental Health) from Canada. U.S. Made prescription drugs are

available in Canada at savings of 30%-60%.

SB 1349: Health Insurance

Rate Oversight

Requires health insurance companies to get

approval for rate increases from the Department of Insurance. The approval

process would require health insurance to justify their administrative costs,

overhead, executive salaries, and profits. The Insurance Commission would have

authority to deny rates deemed unfair or excessive. 26 states have some form of

health insurance premium oversight. As of yet, California has no such review

process.

AB 1958: Prescription

Drug Purchasing Pool

Expands California's purchasing power by

authorizing the California Public Employees\' Retirement System (CalPERS) to

form a purchasing pool for prescription drugs for public and private purchasers.

Allows other California institutional purchasers of prescription drugs, such as

businesses and HMOs, to join the pool and take advantage of the state's

purchasing power to achieve lower prices.

SB 2: Employment Based

Health Care Coverage

The purpose of SB 2 is to assure that all

workers and their families have health coverage by requiring employers either to

purchase that coverage or pay a fee to a state fund that will purchase coverage

for workers and their families.

SB 26: Health Insurance

Cost Control Legislation

California's 6.2 million

uninsured population is projected to grow over the next 10 years unless the

state acts to control costs. SB 26 will require health insurers to prove to

state regulators that rates are not unfair or excessive.

SB 921: The Health Care

for All Californians Act

The Health Care for All

Californians Act would provide health insurance coverage to all Californians

through a single insurance plan offered by the State of California.