Managed Care Introduction -- Managed Care Types -- Advantages and Disadvantages -- How to Choose the Right Plan

Challenges Concerning Medical Benefits -- Relationships to Employee Benefit Wheel -- Web Links Page -- Works Cited

How to Choose the Right Plan

The first step in choosing health insurance is deciding whether to self-insure, purchase insurance through a Managed Care Provider, or some other source. Self-insurance requires an employer to “pay employees’ medical bills directly, employing a healthcare company to act as an administrator” and is generally known as the riskiest model on the market (Unkovic). If an employer chooses to self-insure, the employer must follow federal guidelines set by the Employee Retirement Income and Security Act of 1974 (ERISA). Self-Insured employers are exempt from state regulation according to ERISA as federal law is the supreme law of the land. Therefore, self-insured employers are exempt from state “reserve requirements, mandated benefits, premium taxes, and consumer protection regulations” (Kaiser). States impose heavy regulation and taxation on insurance companies, but are not allowed to do the same with federal plans. As a result, federally regulated self-insurance medical plans are generally less expensive then state regulated plans; however, there is more risk exposure.

Say fifty percent of employees from a large company catch a highly contagious strain of spinal meningitis and must be hospitalized. The net result could be detrimental to the company, perhaps even causing insolvency. To avoid catastrophic loss, some companies will self-insure up to a certain amount, and will purchase excess insurance to cover amount beyond what is retained. This can be viewed as a large aggregate deductible of sorts where after the retained amount is met, the excess insurance comes into effect. Excess insurance is a good form of self-insurance insurance, also known as a stop-loss policy, which is relatively affordable.

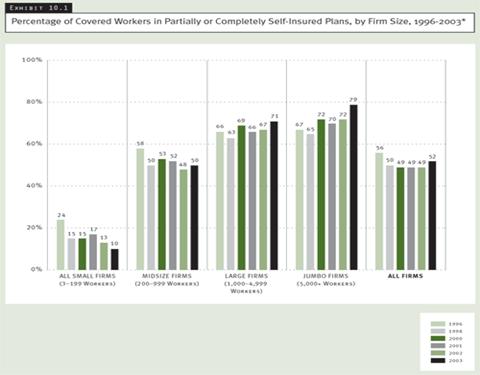

Self-insurance plans are fairly popular. In 2003, 52 percent of insured employees were enrolled in a plan that was completely or partially self-insured (Kaiser). Self-insurance is better suited to larger firms then smaller because of its inherent risk. Spreading the risk over a large number of employees is more economically viable then spreading risk over a few employees; smaller companies likely do not have the financial resources to overcome a catastrophic medical event. According to the Henry J. Kaiser Foundation Family, “The likelihood that an employer self-insures is highly related to the size of the firm. Ten percent of covered workers in all small firms (3 to 199 workers) are in self-insured plans, compared to 50% of workers in mid-size firms (200-999 workers) and 79% of workers in jumbo firms (5,000 or more workers)”- see Exhibit 10.1 next page.

Like most government regulated plans, self-insurance guidelines can be confusing. It is recommended that one talk with an attorney that specializes in ERISA law associated with self-insurance before taking the plunge in this direction. Also, because of strict ERISA guidelines, employers generally contract with a Third Party Administrator (TPA) or an insurance company to act as one. TPAs generally collect premiums, pay claims, and handle other paperwork such as the annual Summary Plan Description or SPD (Ohio Department of Insurance).

The decision to self-insure or purchase insurance must be based on an evaluation of the comparative costs and benefits associated with each. Comparative risk might cause a smaller company to purchase insurance to avoid potential insolvency, even though to self-insure could have lower costs in the short run. A larger company may have enough employees and enough capital to effectively spread the risk of a potential catastrophic event, and choose self-insurance thereby minimizing costs.

http://www.kff.org/insurance/ehbs2003-12-chart.cfm

Purchasing from a provider

Group health insurance provides insurance for a large number of employees, dependents, or retirees. Eligible people are covered in spite of their age or physical condition. In general, group health insurance is provided by employers, professional and trade organizations, unions, social or political groups, and governments.

Small group health insurance applies to businesses with a small number of employees, sometimes one or two employees, but usually between three and twenty-five. As many as one hundred employees may qualify for small group health insurance. Prices on small group health insurance are determined based on two criteria: the expenses of medical services are in a restrictive area and small group health insurance is in a planned operation of services.

Advantages of purchasing from a provider

Providing health care coverage helps attract and retain competent employees. Even if employers require employees to pay their own premiums, the rate is usually lower than that of an individual plan and can be deducted from a tax-free medical expense account established by the employee. The employees also benefit by not having to physically qualify for the coverage. The main reason for an employer to purchase group health insurance is self-preservation; because providing health care benefits is conventional and expected, competent employees will seek employment elsewhere or demand a higher wage to offset their insurance premiums if their employer does not provide health insurance. High job turnover and position vacancy are extremely expensive to businesses in terms of lost work capacity. Additionally, the insurance premiums are tax deductible for the business and the benefits can be viewed as additional, untaxed income for employees. Providing benefits also improves corporate efficiency because the employees tend to be happier and healthier and have higher work productivity.

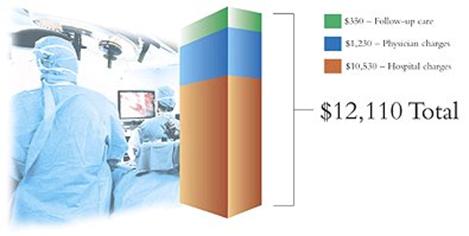

Health coverage also protects against the high financial exposure that may accompany even common accidents or illnesses. Consider what the cost of a typical hospital stay may be (3 days and 2 follow-up visits): **Figures are for illustration purpose only. Actual costs may vary. (Why)

In general, small group health insurance is more reasonably priced than individual plans. It is less expensive because fixed costs are distributed over a larger number of policies. Premiums are even lower for large group health insurance.

Small business health insurance allows the “spread of financial risk between all the members,” which enables members to simultaneously pay lower premiums and expand plan coverage for employees.

Small business health insurance is applicable as long as the employer has two or more full-time, taxable employees (www.healthins.indepth.com).

Disadvantages of purchasing from a provider

In 1997, a survey by the American Health Care Association revealed that less than 6 percent of eligible employees buy group long-term health care insurance. The reason for the low rate of group health insurance participation is the “adverse selection,” which means that the majority of the people who sign up for health insurance have pre-existing health problems and file numerous claims. As a result, group long-term care insurance companies raise rates relative to individual plan rates to cover the higher group claim rates and payments.

Purchasing insurance from a provider can be costly due to high overhead: “printed literature, pay company sales representatives, provide enrollers, maintain help phone lines, provide service personnel to handle problems and maintain a claims department.” Lower net income (premiums minus claim payments) results in an increased percent paying the fixed overhead costs. The effect of the group policy is a smaller benefit than for individual plans at the same cost. Large group premiums are normally between 30 percent and 100 percent higher than individual coverage (Day).

Small businesses are also disadvantaged in purchasing from a provider because health care premiums are lower if the business is paying for more employees.

One of the main disadvantages of group health insurance is the restriction of plan choices for employee selection, i.e., if a company offers only an HMO program, employees have no choice but to take what is offered.

Guidelines

The local chamber of commerce can provide information about community group insurance purchasing pools. State insurance departments are another source for finding an insurance provider (Strength).

This information, compiled by the Institute for Health Policy Solutions, is current as of April 2001. It focuses on groups that offer recipients a choice of health plans.

|

State |

Plan |

Size of Firm |

Region |

Phone Number |

|

California |

Pacific Health Advantage |

2-50 employees, or employers of any size if they obtain coverage through a qualifying trade association. |

Statewide |

(949) 766-1905 |

(Strength)

Employers should consider using a state-licensed broker for group health insurance purchases. Brokers can guide employers in finding suitable group health insurance for their employees. Registered Health Underwriters are brokers who have completed required coursework and passed exams dealing with the health insurance industry.

Needs and Wants of Employees

Some health plans offer a network of doctors. If employees have personal family doctors they wish to keep, additional costs might be incurred to accommodate these preferences, or visits to these doctors might not be covered at all.

Some health plans will not allow you to go out of network for coverage, meaning that employees must pay completely out-of-pocket for being seen by a doctor that is not on a given list of providers. However, out of network coverage can usually be added at a cost.

Preventive services vary for each provider; adequate check-up exams should be included in desirable insurance plans.

Prescription drug benefits are very important for employees; the prescriptions that are and are not covered vary by provider and plan choice. Employers should try to provide the maximum benefit to employees by selecting a plan that will provide prescription benefits the majority of employees.

Cost of group health insurance for employees is always a big concern. Higher co-payments decrease employee premiums. Co-payments are a form of cost-sharing that require insured people to pay a fixed dollar amount for a received medical service. Increase deductibles are another way to lower employee out-of-pocket costs. Deductibles are a fixed dollar amount which an insured person pays before the insurer starts to make payments for covered medical services during the benefit period, usually a year (Group).

Requirements for Employers

Requirements differ by the various health care insurance providers. In order to qualify for a group plan such as Athem, the employer of the company must provide a copy of the state and federal tax form to show proof of his/her legal business, home-based employers must show proof of working at least 30 hours per week at his/her business, and employers must provide evidence of running a business for three consecutive months (http://moneycentral.msn.com).

Requirement for Insurers

Insurers are required to check that the members of the company who are purchasing health insurance actually work for the employers. In addition, various documents are essential for sole proprietors to provide to the insurer or health plan administrator on a yearly basis. Deciding how to implement a medical benefits program is not as easy as understanding the similarities, differences, advantages, and disadvantages of each type, there are many other challenges facing employers and employees with regards to medical care packages.